Pexapark: European BESS marketplace maturing as sophisticated contracts go mainstream

With the economics rapidly evolving and initial opportunities particularly profitable, front-of-the-meter battery marketplaces are dynamic places. With the need for batteries to “flatten” the production curve of renewables as solar and wind displaces thermal generation in an increasing number of European countries, the price signals for accelerating utility-scale battery deployment are evident.

Encouragingly, growing levels of sophistication in terms of offtake or usage contracts for grid-scale batteries are paving the way for battery projects to attract debt financing – accelerating deployment. Experts from Pexapark reported the trend this month when presenting the findings of their Renewables Market Outlook 2025 report.

Mathieu Ville, the vice president for PPA and BESS transactions at Pexapark says that he is seeing the appetite for sophisticated “battery structures” emerging from both battery project owners and operators, like optimisers, in some parts of Europe, clear signs that the marketplace is maturing.

“I think, indeed, it would be the moment where those battery contracts start to become mainstream,” Ville tells ESS News. “Once you have a proven set of structures, then maybe it is a sign that we have seen so many of these battery structures that we are now getting into very sophisticated territory.”

Source: Pexapark

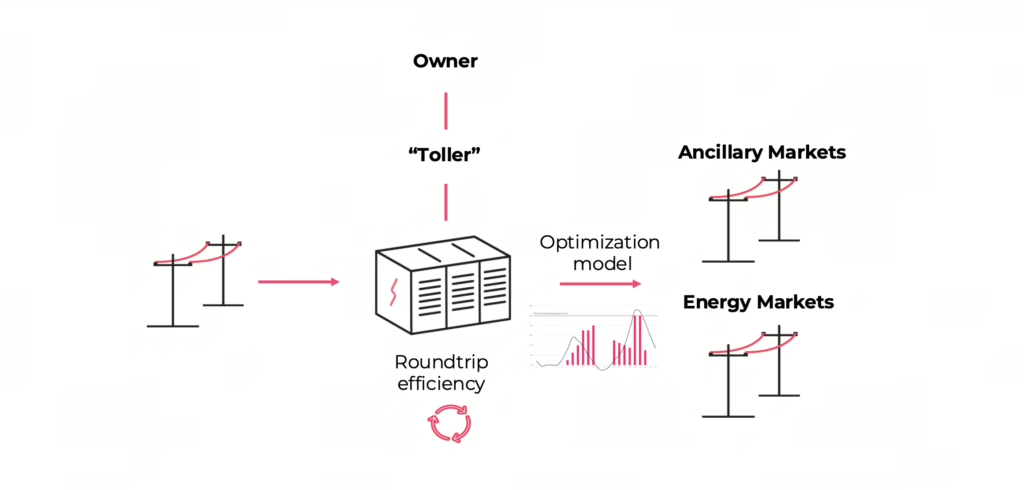

Battery structures

The financial structures with which batteries are being developed were summarised by Pexapark in their 2025 report. They include “tolling”, “floor”, and “merchant” – each with varying levels of risk and potential upside for both the asset owner and operator.

Ville reports that while tolling is more commonplace in the early stages of utility-scale BESS market development, it is becoming superseded by potentially more profitable structures in relatively advanced European battery marketplaces like the United Kingdom.

Tolling refers to an agreement whereby the battery project owners contracts the operation of the asset for a set period of time to a third party, namely an optimiser. The optimiser can then utilise the battery asset in both ancillary and arbitrage applications.

“Tolling is very bankable, it’s very robust, and it does allow debt financing. Tolling was, in the early days when you didn’t know how much ancillary services [revenue to expect], very interesting because it enabled so much profit from the battery owners. I feel now it is pivoting more towards floor, as the offers from optimisers and utilities have changed drastically.”

Floor structures allow for a sharing of the upside between the owner and optimiser, above a base level of guaranteed revenue. The base, or floor, ensures sufficient revenue for the securing of debt financing.

“The floor is generally set way below what you think you will get [from the market, in terms of revenue] and anything above is shared between the battery owner and the optimiser,” explains Ville. Within floor contracts, mechanisms such as “day-ahead swaps” are being explored by European market participants, the Pexapark expert adds, although these are relatively nascent.

Merchant, for investors with a higher tolerance for risk, can prove attractive when the trend towards strong battery revenues is clear – on the back of high levels of market volatility. “Merchant is upcoming,” says Ville. “We think merchant might work going forward for bankability purposes.”

Source: Pexapark

Positive development

While complex, the increased sophistication provides opportunities for investors as batteries begin to exhaust earlier revenue streams due to market saturation, says Alexa Capital co-founder and partner Gerard Reid. Although timing remains crucial.

“Tolling is giving away significant upside,” says Reid. “Now that the pricing in the [UK battery] market has gone down, it means the tolling price is going down. Then it doesn’t make sense to toll because you’re giving away this upside.”

Reid adds the US state of Texas and Germany were “the two big battery markets” in 2024, however he warns profits can evaporate when the arbitrage opportunity abates. “You have to get in there early to benefit from the trading inefficiency.”

Pexapark acquires RenewaFi

Texas saw rapid grid-scale battery deployment in 2024. Energy data intelligence provider Grid Status finds that more than 10 GW of big batteries were operational on ERCOT – representing a year-on-year doubling of capacity. Much of this capacity supplies ancillary services markets, Grid Status notes.

This week, Pexapark announced that it had completed the acquisition of RenewaFi, a PPA and battery toll advisor active in the ERCOT region. The acquisition signaled Pexapark’s U.S.-marketplace entry.

“RenewaFi brings a highly complementary business, a strong US network of nearly 200 energy companies, vast amounts of high-quality price data, and a trusted marketplace for PPAs and BESS tolls,” said Pexapark co-founder Luca Pedretti in a statement.

Echoes of PPA

The expansion of both the available marketplaces and investment opportunities for front-of-the-meter batteries augurs well for future development – particularly as the need for flexibility on electricity networks increases. And the development echoes the renewable PPA market evolution.

“There were plain vanilla PPAs in the early days, and once the appetite for those is exhausted, you start to begin going off menu,” says Pexapark’s Ville. “It’s also a good thing for investors because the playing field becomes wider as you have plenty of options.”

Tolling or floor contracts need not encompass all of a battery project’s capacity. Part of the battery can be covered by an agreement with an optimiser, facilitating finance, while the remainder used to exploit energy-market opportunities. “It seems to be becoming a more-and-more common approach,” says Ville.

Additionally, falling battery costs will continue to enhance grid-scale BESS competitiveness, notes Reid. “The cost of batteries is continuing to fall and the management of those batteries is improving. We’re probably going to see another 20 to 25% fall in cost meaning the business case improves year after year. It’s incredibly interesting what’s going on.”

Written by

")

Popular Posts

")