BBDF 2026: finance, tolling, and getting the merchant balance right

")

Finance took center stage at BBDF in a lively session covering the range of funding options available to BESS projects.

Mark van Zon, senior director at ABN AMRO, opened the session by introducing a host of financial concepts such as floor contracts, gearing, mini-perm loans, balloon management, and aspects like cash-sweep mechanisms.

Panelists included banks, offtakers, and developers delved into the detail as industry experts shared first-hand accounts of European BESS financing. Mikko Preuss, chief commercial officer at Terralayr represented developers, alongside bankers Marcus Starke, director energy origination at NORD/LB, and Mark van Zon. Nils van Afferden, asset originator, flexibilities and batteries at RWE, was also on stage to share the offtaker perspective.

How much merchant is bankable?

Should projects have more or less merchant revenue? The panel largely agreed on securing more contracted revenue through tolling, but some argued in favor of a balance between the two.

How much merchant revenue can a BESS project retain and still be bankable? Marcus Starke explained how some common structures strike the balance. “Typical structures are 12-month merchant phases, then around 80% tolling for five to seven years. This works for projects with high gearing.”

“We are not opposed to merchants,” added van Zon, but he noted that lenders do want and need to be protected. “It can work, but it takes a little extra care,” he said, adding the bank had even financed a 100% merchant project, but with lower gearing and additional protections.

Marcus Starke said NORD/LB had also already backed a full merchant project in the United States, but he added it “was not working well at the moment”.

Speaking from the offtaker side, Nils van Afferden said banks have required more predictable revenue. Tolling provides this, but van Afferden also mentioned the role credibility plays alongside long-term revenue guarantees. “Being a credible partner is also important,” said van Afferden, in relation to the toller’s role as a long-term partner.

Preuss from Terralayr said that when discussion turns to tolling, revenue is the focus – but there are also cost implications that should be considered. “It was an important realization for us as an [agreed toll] doesn’t mean risk-free mode for a battery. It mitigates a portion of risk, namely market exposure, but increases risks on the other side like delivering megawatts and efficiency and so on. Or there’ll be sanctions, most likely. This was a big topic of consideration when considering start dates, COD dates and so on,” he said.

Session moderator Ann Cocquyt, director – PPA and BESS Transactions at Pexapark, added that she’d seen companies underestimate complexities in these projects, with the panel in general agreement.

On the risk facing tolling offtakers, van Afferden was matter of fact about what’s involved when committing to a price. “There is sometimes a misunderstanding of what a tolling agreement is about. The main thing is to secure revenues and reduce merchant risk. But you cannot take away all risks, like risks of curtailment … we price in what we can, but you can have mark to market penalty or compensation. There are different ways to structure, but it always boils down to risk for each party and what can be accepted.”

Van Zon noted that due diligence goes far beyond understanding a tolling agreement, even expanding to long-term service agreements (LTSAs) and EPCs, warranties, and more.

Marcus Starke added that there is often a misunderstanding that tolling is risk-free. “Having merchant notes is also beneficial,” Starke said. “Some buffer is required, such as if availability is not always able to be met. That’s why we always say don’t go 100% tolling. Margins and ratings drivers and pricing profiles, it’s a difference if you have a flat price vs a shaped price. Negotiating a good tolling contract takes time, and you need good lawyers that have seen such tolling agreements.”

Other panelists agree that a merchant buffer – retaining a segment of the overall capacity for trading – is important. Mikko Preuss shared a developer’s perspective on the issue. Preuss explained that having some merchant buffer means unsold energy and unsold commitments from a battery, which can allow for upside, and can also help protect against penalties with tolling if there appears to be downsides. How this can be done depends on technical aspects, such as virtual tolling and more.

Preuss also advocated for small, distributed projects to avoid risk presented by geography – not just having large batteries in one place. He added that as part of his company’s offering, technical solutions can aggregate batteries and slice them between multiple offtakers to spread across revenues and risks.

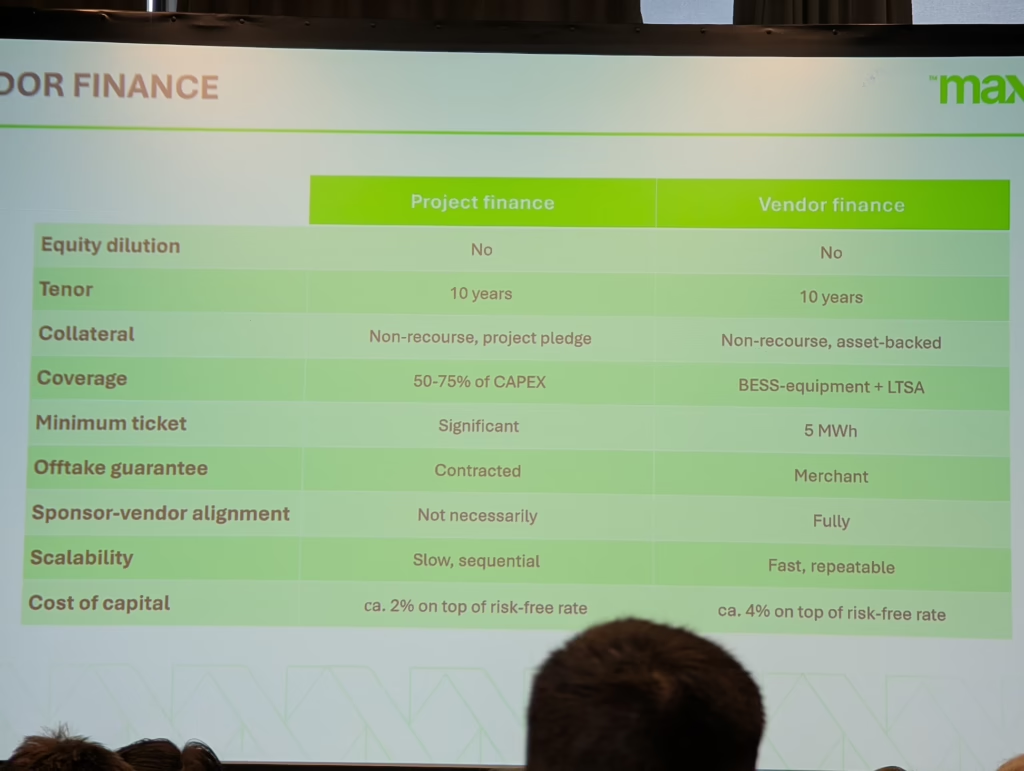

Vendor financing as an alternative

Ruben Valiente, managing director at Maxxen Energy offered another option for project financing. Presenting between panels, Valiente said the battery storage aspect of a project now costs approximately €100/kWh, inclusive of the DC block, PCS, EMS and more – which is around 70% to 80% of the total cost of the project.

He explained vendor financing in relation to cars, where Valiente said: “The vendor will produce and supply the equipment initially for free, but it’s not free.”

In a simpler form of contract, Valiente said Maxxen charges a €1/kWh activation fee, delivers all BESS equipment, and there is a fixed lease fee after COD each quarter, with a fee that can be structured as either flat or tiered. The contract includes terms around O&M and LTSA + Performance Guarantees, and at the loan tenor end, the project owns the equipment.

Valiente said this could be more advantageous for smaller projects where there is a funding gap, and detailed how contract revenues may work and coverage ratios could remain safe. He mentioned that a project where money hasn’t been paid is less concerning due to the battery asset. “I’m an industrialist,” said Valiente, adding that batteries in default can be decommissioned, moved to a new project, and installed again.

Regulatory risk looms large

In a second panel continuing the discussion, new panelists picked up the core themes of the event, again making direct complaints around regulatory risk.

Discussion continued on a second panel, with new expert guests putting risk under the microscope.

The panel was asked “who should take the merchant risk” and Maxime Nekoian, finance director, Gresham House, argued risk is on the equity side, and emphasized the need to enter some portion of storage into a tolling agreement to even out the risk.

He added that the fund is currently raising $1 billion to invest in Germany, despite the regulatory concerns facing the market’s utility-scale BESS segment.

Alexander Drousiotis, vice president, structured finance energy, Santander Corporate & Investment Banking, said: “You inevitably need tolling agreements, in part, to spread the risk … We see more and more people moving away from pure merchant exposure at the moment.”

Grace Kankindi, deputy head of investment management, Aquila Clean Energy, described the clean energy business as an early mover. “And early on, we went equity only,” Kankindi said. “Beyond merchant risk, we have to look at what makes a project good – like a quality optimizer, for example.”

Coen Hutters, energy transition specialist at Rabobank, emphasized repeatedly the potential issues that regulatory change and upheaval in Germany could cause, suggesting it is bigger than merchant risk.

“The energy market is a good example of how difficult banking can be,” he said, detailing how banks deal with risk calculations. “You just have to see the news today to see how volatile and uncertain energy is. More and more the focus is on resilience and energy security and affordability. How do those prices that batteries rely on unfold? We’re talking merchant risk, and we can show scenarios for prices rising and falling, and markets saturating and when, but even more relevant, is regulatory risk. Will batteries have to pay grid fees, potentially retroactively? That’s really what is making it difficult.”

Hutters added that regulatory clarity can improve the investment picture, mentioning that Spain’s regulatory environment is now improving and supporting investment and new battery projects after years of less attractive and at times unclear policy.

Panelists agreed on several further points, such as regulatory risks and the concepts of retroactive grid fees being difficult. They also agreed that agility in the market matters, as factors and regulations change. Fast movers can both take advantage of or seek to exit markets rapidly.

Written by

Comments

")

")

Popular Posts

")