Arbitrage remains leading use case for US grid-scale batteries

")

The latest data from the U.S. Energy Information Administration (EIA) confirms that arbitrage – the practice of buying electricity when prices are low and selling it when prices are high – remains the dominant use case for utility-scale battery energy storage systems in the US.

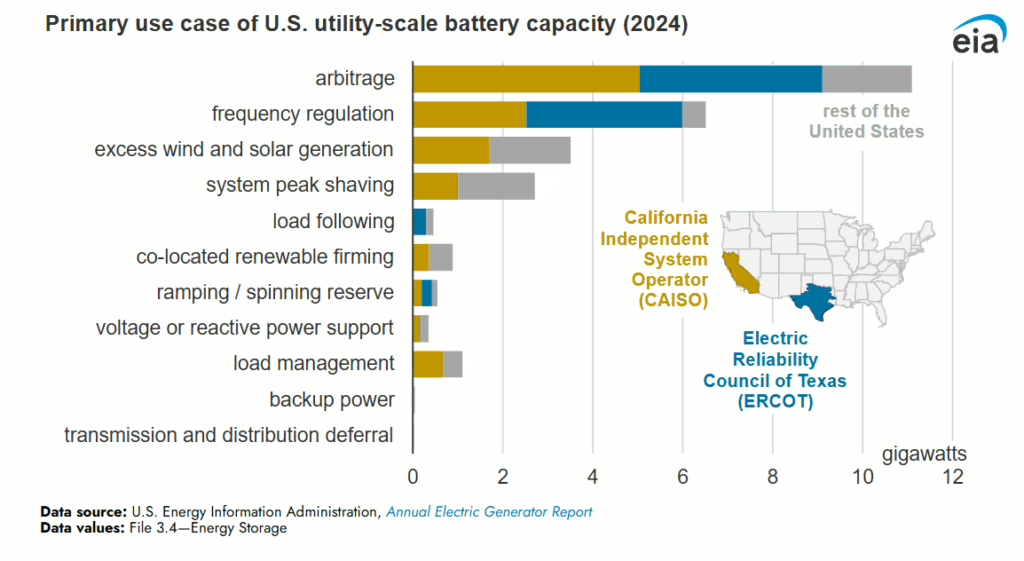

In 2024, operators reported that 66% of all utility-scale battery capacity included arbitrage among its applications, while 41% of total capacity was used primarily for arbitrage.

The next most common application was frequency regulation, which was the primary use for 24% of battery capacity. Frequency regulation plays a critical role in maintaining the grid’s stability by keeping it operating at a steady 60 cycles per second.

While this breakdown is similar to 2023 – still with arbitrage leading the way – it’s a notable shift compared to earlier years, when frequency regulation was the most commonly cited primary use of battery systems.

This transition reflects a broader trend seen in mature energy storage markets, such as the UK. As ancillary services markets tend to be relatively shallow, a shift from frequency regulation to energy arbitrage is a natural evolution as battery deployment scales.

The most significant change in the US is occurring in Texas, where battery operators are increasingly depending on energy arbitrage as their main revenue stream, rather than ancillary services.

According to Modo Energy, in 2023, 85% of BESS revenues in Texas came from ancillary services. By 2024, that number had dropped sharply, with nearly 60% of revenues coming from arbitrage – a clear signal of market maturation and shifting economics.

Growing fleet

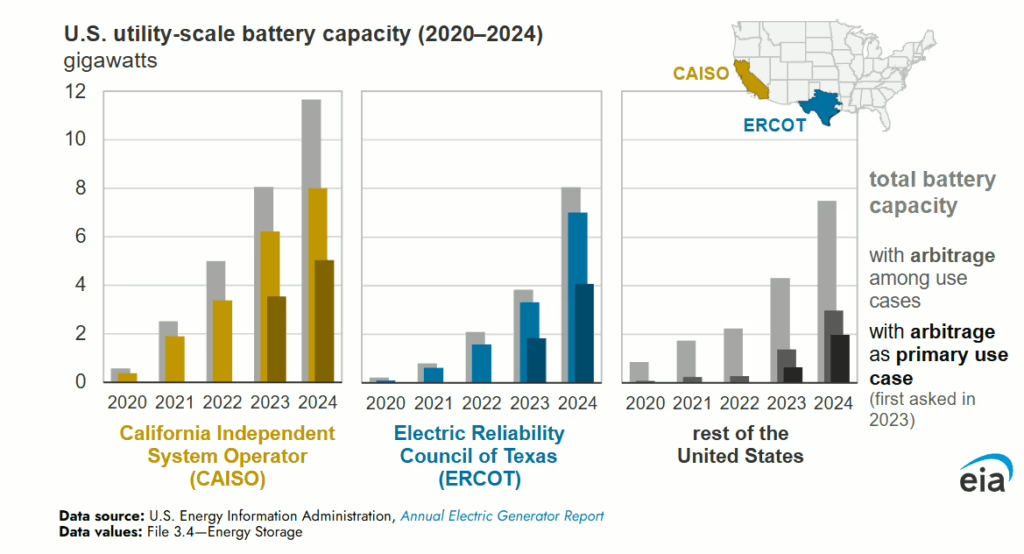

The majority of the US utility-scale battery capacity is concentrated in California and Texas, within the CAISO and ERCOT markets.

As of the end of 2024, CAISO reported 11.7 GW of installed battery capacity, 43% of which was primarily used for arbitrage. Meanwhile, ERCOT reported 8.1 GW of capacity, with 50% primarily used for arbitrage.

That’s up from 8 GW in CAISO and 3.9 GW in ERCOT at the end of 2023. Despite the rapid growth, the share of capacity primarily used for arbitrage remained consistent year-over-year.

Nationally, by the end of 2024, the US had approximatel 11 GW of grid-scale battery capacity with arbitrage as the top use case. Around 6.5 GW primarily dedicated to frequency regulation.

Beyond arbitrage and frequency regulation, utility-scale batteries in the US are also being used for a growing number of grid-support applications, including: absorbing excess wind and solar energy, system peak shaving, load following, co-located renewable firming, ramping/spinning reserve, voltage or reactive power support, load management, backup power, and transmission and distribution referral.

These evolving applications underscore the increasing versatility of battery energy storage systems and their expanding role in grid stabilization.

Written by

")

Popular Posts