BBDF 2026 opening session: optimism, caution, and grid fees

Europe’s battery storage has matured, but remains dynamic with strong growth across markets.

That was one of the key takeaways from the opening session of the Battery Business & Development Forum (BBDF) 2026 in Frankfurt am Main, Germany. Now in its second year, the two-day event welcomes more than 100 expert speakers and 28 sponsor partners for insightful sessions co-hosted by pv magazine and ESS News, Solar Power Europe, and Connexio PSE.

Attendees in the first BBDF session heard how even amid global uncertainty, investors believe more capital will come to the energy storage market. Yet there were cautionary remarks to regarding regulatory risk, with ongoing dicussions in Germany around charging existing and new BESS project grid fees for market access serving as an example.

Walburga Hemetsberger, CEO of SolarPower Europe, mentioned the energy crisis and the ongoing policy response in Brussels, and reminded the audience that Europe needs 10 times as many batteries as it has now by 2030.

Christoph Ostermann, CEO and co-founder of green flexibility, opened the session as the first speaker, offering perspective from his company’s work as developer and BESS operator. Ostermann noted that tailwinds for the industry have started to turn into headwinds. He highlighted examples in the German market such as regulatory issues and potential grid fees.

“Grid access remains a key bottleneck,” said Ostermann. “And it’s a question of access, but quantity and quality. It’s harder to get access, but the quality is also more constrained, which is heavily influencing usability for BESS. Along with longer timelines, all of this has consequences for the business case of BESS.

“Still, the core thesis of our market remains there. BESS is the most versatile, and the most flexible, and in many cases, also the most economic. The situation in Iran reminds us that renewable energy is not just economic, but about resilience.

“We also see that the market is moving towards co-operation. Instead of the ‘wait and see’ and waiting for a storm to blow over, the marketplace is widening. We are getting more inquiries and offers for co-development and to bring projects such as ready-to-builds to COD together. We look with optimism into the future, we understand that’s why forums such as this are so important, as it provides the platform we need.”

Asked for his views on if regulatory pressures might cause plans to change, Ostermann had a concrete answer for BBDF attendees.

“I know it for sure, because we changed our plans for this year! Everything takes longer and is more difficult. With grid fees uncertain, economic calculations to base an investment decision on is quite a challenge.”

BESS macro trends

Seven macro trends for European BESS were then brought into focus by Anna Darmani, principal analyst, Wood Mackenzie.

Darmani reminded the audience that Europe’s energy storage is currently defined by its distributed segment. Wood Mackenzie estimated 48 GW of total storage is deployed in Europe, excluding pumped storage. Distributed storage makes up 62% of that figure, according to the analyst, with the remaining 38% from utility. The utility segment is growing rapidly, however, and Darmani shared a chart showing installed assets and operational hours, with bubble sizes proportional to storage capacities that highlighted the trend clearly for BBDF guests.

Growth in -co-location was also highlighted by Darmani as a key BESS trend, driven by grid scarcity and declining wind and solar capture prices. The Wood Mackenzie analyst reported 3 GW of operational capacity with 22 GW in the pipeline. Darmani reinforced the case for greater energy storage deployment by showing county of negative prices across electricity market segments, and made the case that BESS could play a role in alleviating issues here while supporting falling capture prices.

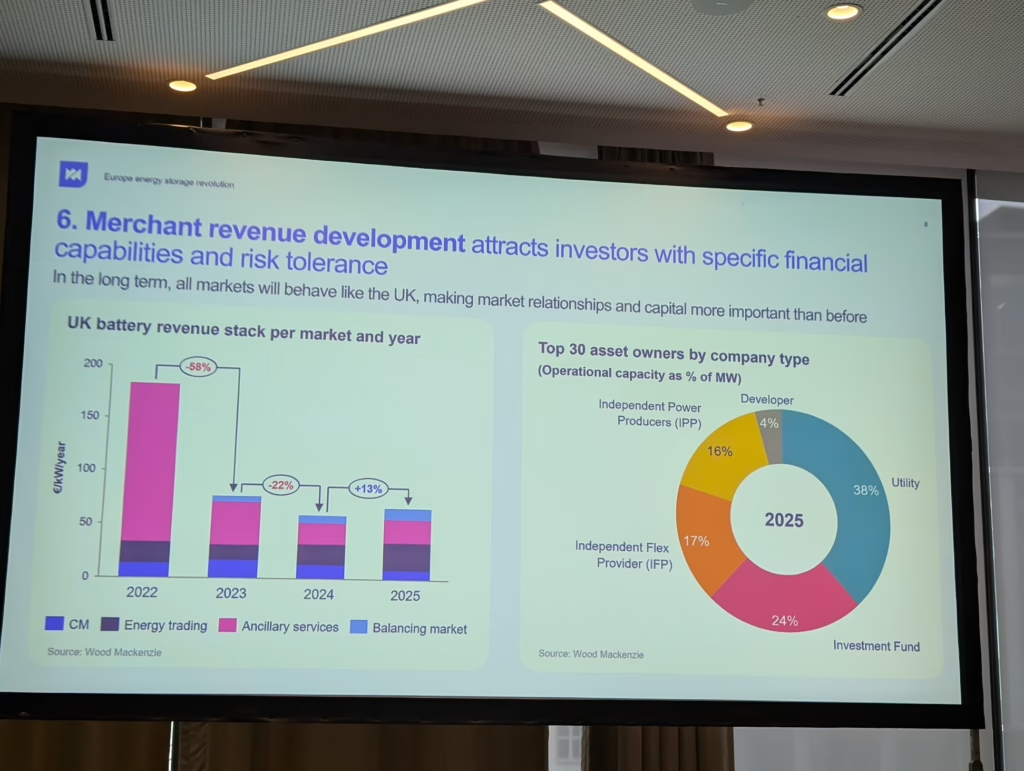

When Wood Mackenzie is asked about merchant revenue developments, Darmani said it points to the United Kingdom as the direction of travel. The UK BESS market has already been through the cycle of falling revenue from ancillary services, forcing projects to adjust with other sources of revenue.

Battery contracting was also addressed, with Darmani noting the landscape is shifting as more renewable projects opt for storage offtake contracts to hedge against merchant risks.

Darmani was also asked about other factors that can support BESS projects, and the analyst highlighted the crucial role government auctions and tenders play in developing BESS in emerging markets, even when merchant revenues look good. She also noted that while geopolitical risks, uncertainty and volatility can actually be good for energy traders, how prices for batteries from China develop will be critical, even the long-term trend is downward.

Panel talks risk

Allianz Global Investors (AllianzGI) and TotalEnergies kicked off a panel discussion on BESS investment with a reminder of a major new deal. AllianzGI recently acquired a 50% stake in a portfolio of 11 under-construction BESS projects from TotalEnergies, a first direct equiry investment of its kind with a cumulative power total of around 789 MW/ 1,628 MWh. The estimated investment is €500 million ($581 million), with approximately 70% financed through debt.

Asked about why this new partnership happened, Yann Laot, director M&A, TotalEnergies, noted that the quantity of capital that can be deployed at any time is limited.

Moving on to how the partnership came together, Tim Danis from Allianz GI credited TotalEnergies for delivering a comprehensive financial blueprint and noted that their full view of the ecosystem could build trust. Danis added that while partnership discussions began some time ago, negotiating the overall risk profile was important.

Laot said that for TotalEnergies, clear governance was an important factor. And when discussing other potential partners for this sale without naming them, he said that while many factors are important, much of what was key to choosing a partner remains a key for him for the ultimate choice of the partner relies on what is “not written,” sharing the example of how both parties were able to handle surprises u such as markets and prices changing overnight. The choice of partners therefore relied at least partially on mindset, while planning for very long-term partnerships.

German grid frees

German grid fees were expected as a topic of discussion aross the two days, and investors on the panel were critical of what’s been proposed. There was less criticism for fees applied to future projects, but a strong negative sentiment toward fees for projects already established, or under construction.

Nadiya Vargola, head of BESS business development at Alpiq AG, said grid fees being applied retroactively would be “unheard of” and “dangerous”.

She added: “I can’t say this would stop investments, as BESS is needed, especially in Germany, where curtailments are significant. But regulators need to understand these changes are significant and I hope regulators are in the room!”

Yann Laot offered a similar assessment, noting ongoing regulatory stability can be more important than economics. “Whatever the final value [of potential grid fees to come], it’s easier to make a final investment decision when your business case is known,” Laot said.

Jeroen Zanders, managing director, Macquarie Capital, added that some level of grid fees can be handled in modelling, but retroactive moves would be unexpected.

Merchant risk

Vargola noted that the cost of BESS is going down while maturity is increasing, which does create a dynamic market. But she also said there is more nervousness in the market around merchant risk. “Saturation in markets is happening quicker than expected, meaning players are trying to see how secure their business cases are,” she said.

AllianzGI’s Danis said unit economics speak for themselves but added there are many things that can and will go wrong. “Grid fees pose a major risk, and I see a lot of market irritation about them. Second, the availability of an asset, availability and uptime are prerequisites, which adds further hurdles as you can’t plan for it, and in addition, there is no compensation. Then, we are entering a period where projects are not bankable and will fail,” Danis said.

On the question of the “right” level of merchant risk, Laot suggested that some merchant risk is like salt in cooking, which was paraphrased as “A little risk, like salt, creates taste. But too much and it’s not tasty at all.”

Zanders shared exampled of real projects: “From Macquarie’s side, in Australia, we did a 20-year, 100% off-take with with Shell. On the other hand in the Netherlands, we structure it as almost 100% merchant. I do think in general, you see the market moving to 50-70% tolled or floored, roughly. Otherwise, we go to fully merchant, and you get to quite aggressive PE funds or even hedge funds.”

Asked if more capital would be coming to the market over the next 12 months, Danis said that while there are multiple factors at place, he believes further capital will come. Vargola agreed, noting that the market fundamentals are there, and BESS is needed for energy independence – as highlighted by the ongoing conflict in Iran.

Battery Business & Development Forum 2026 is being held across March 31, April 1 at Meliá Frankfurt City.

Written by

")

Popular Posts

")