CEA: Trade barriers set to see U.S. BESS prices increase 35% in 2025

While battery makers delivered price declines of more than 20% last year, in the US marketplace 2025 looks likely to see prices head in the other direction on the back of tariffs. While uncertainty persists as to which tariffs will impact the battery market most significantly, Clean Energy Associate (CEA) conclude that prices of BESS from China are likely to increase by 35% this year.

CEA published the finding in its annual ESS Price Forecast report, which was released this week.

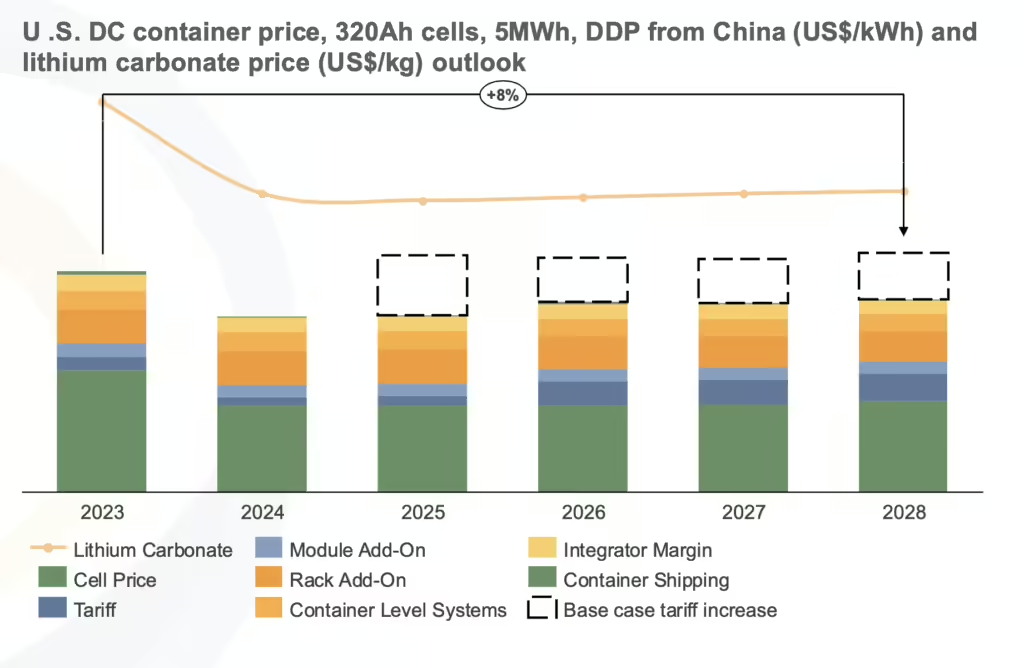

In its 2025 pricing analysis, CEA noted that there is a lot of uncertainty as to how US tariff policy will play out. However it concluded that BESS prices in the country will be “above typical prices in 2023 in the base case.”

Multiple trade barriers

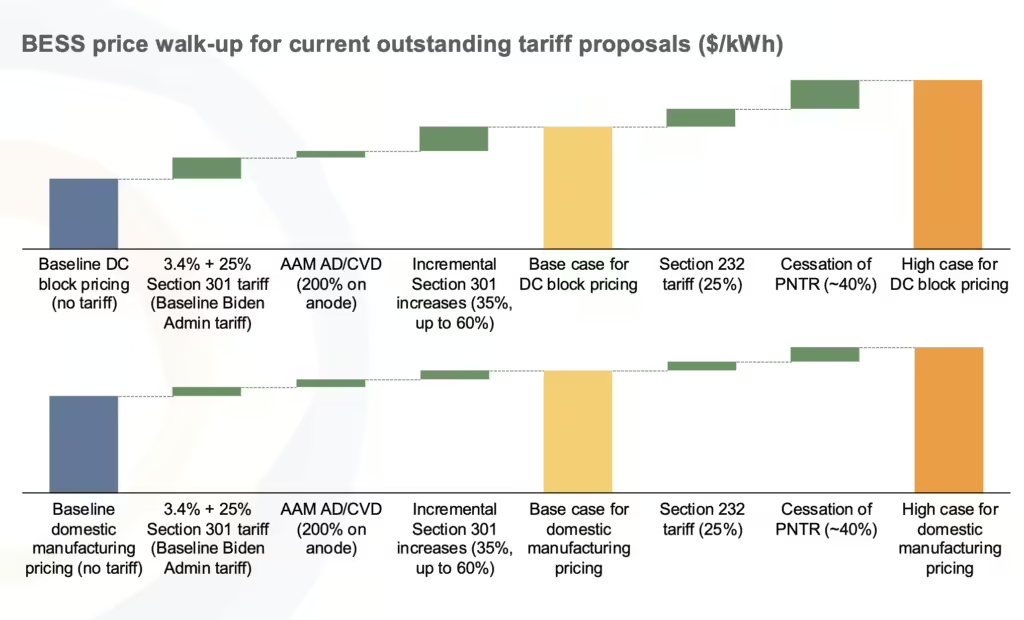

There are a host of tariffs and duties set to impact the US battery industry in 2025: Section 301 tariffs have been in place since 2019, there are hefty AD/CVD duties on anode active material, and section 232 tariffs on imported aluminium and steel, which were imposed during the first Trump Presidency in 2018.

Further complicating matters, legislation to revoke China’s Permanent Normal Trade Relations (PNTR) status, which provides the country with preferential tariff treatment, was introduced into Congress in November. CEA observes that the bill to wind back China’s PNTR, the Restoring Trade Fairness Act, “has a good chance” of being held up in the Senate.

“The continuing complexity of the situation, especially given that only half of these potential tariffs would originate from the Executive Branch, makes it important to illustrate the range of potential outcomes,” writes CEA in its analysis.

Diversifying supply chains

With lithium iron phosphate (LFP) battery production almost exclusively located in China, the US tariffs are effective in pushing up the price of battery packs in the country. And a non-Chinese LFP supply chain is still some years away. The only “viable BESS procurement options,” writes CEA, are locally integrated systems using Chinese LFP cells, or Korean-made nickel manganese cobalt (NMC) cells.

“US, Southeast Asia, and Korean LFP manufacturing will only become options in the 2025-27 timeframe,” writes CEA. BESS using Chinese-made LFP will remain the cheapest over this timeframe, the analysis concludes.

While domestically produced lithium ion battery cells are still some way off, the integration of imported batteries into systems in the US will avoid some tariffs.

“Batteries integrated in the US from imported parts would only see tariffs on those components imported from China,” writes CEA.

The US is the second biggest BESS market globally, behind China. BloombergNEF expects installations of around 13.5 GW/48 GWh to be realized in the US this year, representing relatively modest annual growth of approximately 5.5%/13%.

Vertical integration, market concentration

While some manufacturers are seeking to serve US BESS demand by localizing at least part of their production, others are expanding further downstream into the system integration business. The world’s largest battery producer Contemporary Amperex Technology Co. (CATL) has embraced vertical integration. It introduced its Tener containerised system to the market in 2024, which has a capacity of 6.25 MW.

“CATL is vertically integrated, and will also be a cell supplier to other players,” BloombergNEF’s Yayoi Sekine, who heads up the company’s battery research, told ESS News. “A lot more of the cell manufacturers, because prices have gone down so much, are trying to become an integration business. And then a lot of the integration business companies are trying to do more or be closer to the cell manufacturing side.”

Korea-based market researcher SNE Research found that CATL captured 35.6% of the EV battery market in 2023, with 308 GWh of shipments. It notes that the manufacturing landscape is highly concentrated, with the top-10 battery manufacturers accounting for 94% market share, and within that, the top-5 captured 78.4%.

CATL has been under a regulatory cloud in the US in 2025. This month the company was placed by the US Department of Defence of companies that are believed to have links to the Chinese military – a claim CATL describes as being a “false designation.”

Written by

")