BloombergNEF confirms record US energy storage additions in 2025, but the pipeline is cooling

")

The BloombergNEF 2026 Sustainable Energy in America Factbook confirms 2025 as a record year for U.S. utility-scale storage at 15.2 GW added — in line with Wood Mackenzie/American Clean Power figures published across the year.

BNEF’s report, produced in partnership with the Business Council for Sustainable Energy, is an 80-page document that comprehensively examines the entire energy system. Focusing on energy storage, despite a volatile policy and trade environment, utility-scale storage in particular was a central component of new power capacity. The report also includes several specific datapoints that haven’t been widely circulated.

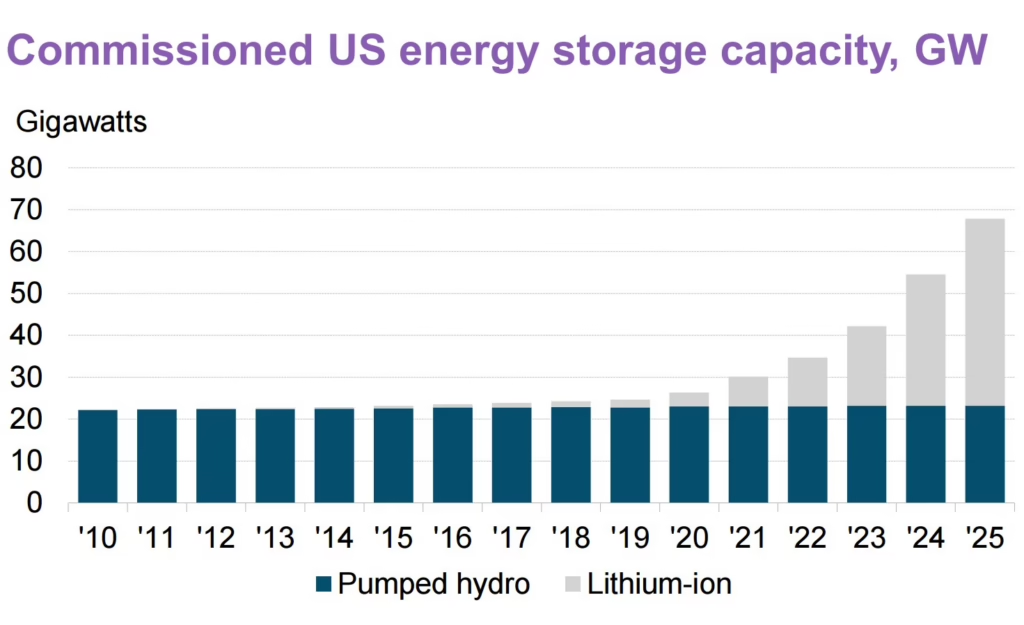

The US commissioned an estimated 15.2 GW of new utility-scale storage capacity in 2025. This represents a 35.4% increase over 2024 and contributed to a total of 53.7 GW of new utility-scale generation and storage capacity, or the highest annual addition in more than two decades. This growth was driven by declining battery costs and the need for system flexibility as renewable penetration rises.

Cumulative non-hydro storage (primarily lithium-ion) reached 42 GWh by year-end. Pumped hydro gets its nod as well, prominent in the chart below, with it accounting for 34% of power capacity but 65% of stored energy within the country, though it has had next to zero additions over the past decades.

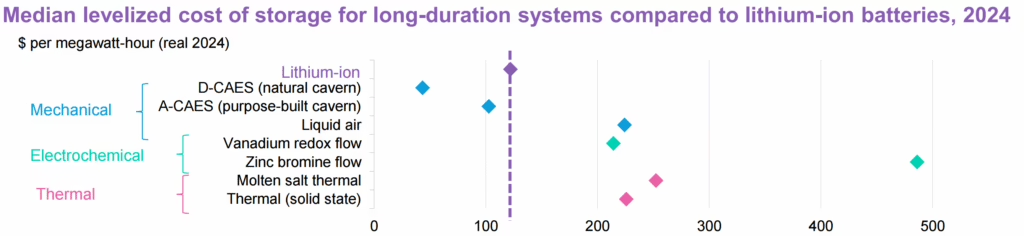

Another interesting chart from the book on page 63 shows the median levelized cost of storage for long-duration systems vs lithium-ion in 2024 terms.

Also as a useful fact: retail electricity prices rose an average of 2.3% nationally year-on-year, though that average suppresses major changes to states like New Jersey, where prices rose a reported 12%.

Policy and Tariff Volatility

Policy changes introduced significant whiplash to the sector. Import duties on non-EV batteries for stationary storage began the year at 11%, spiked to over 156% in April under the International Emergency Economic Powers Act (IEEPA) as desired by the Trump administration, and eventually settled at 31% by December.

This tariff volatility directly altered sourcing patterns. China’s share of US battery imports fell sharply from 69% in 2024 to 40% in 2025 (in dollar terms) as developers adapted to the trade barriers.

The effective rates on batteries frustratingly do shift depending on which tariff layers are included; these figures are BNEF’s best read on the situation versus a final “settled” figure, but they do provide one of the more specific single-source summaries of fluctuating duties, sometimes changing week-to-week. BNEF listed 87 trade and tariff policy changes on energy transition-related goods in 2025 alone.

See more from mid-2025: Turbulent times for US energy storage.

More signs of a slowdown

While total interconnection applications hit 377 GW across the seven major US ISOs, the pace of new storage requests has been slowing. Applications for new storage interconnections declined 20% year-on-year, partly due to grid operator pauses, permitting hurdles, delays, uncertainty, and more. Previously, WoodMac also forecast the year ahead as seeing a temporary slowdown.

On the manufacturing front, US annual lithium-ion battery cell capacity grew 56% in 2025 to reach 295 GWh, though this includes electric vehicle battery manufacturing. In terms of stationary storage, BNEF analysts also noted the moves made by the EV battery industry, where unexpectedly slow EV sales have seen manufacturers like Ford and LG Energy Solution and co allocating their factory domestic capacity specifically toward stationary storage production. See NextStar in Canada and Ford in Kentucky and Michigan.

The Impact of OBBBA

The One Big Beautiful Bill Act (OBBBA), signed into law on July 4, 2025, has reshaped the landscape for incentives and therefore the direction of various renewable industries. For energy storage, it retains a 30% Investment Tax Credit (ITC) through 2034, but projects must now meet increasingly stringent Foreign Entity of Concern (FEOC) rules regarding supply chains to qualify. Projects starting construction after 2025 risk losing credit eligibility if they remain reliant on components from prohibited foreign entities.

These are still tricky: developers need to rethink diligence, serviceability and replacement strategies to avoid failures of FEOC rules.

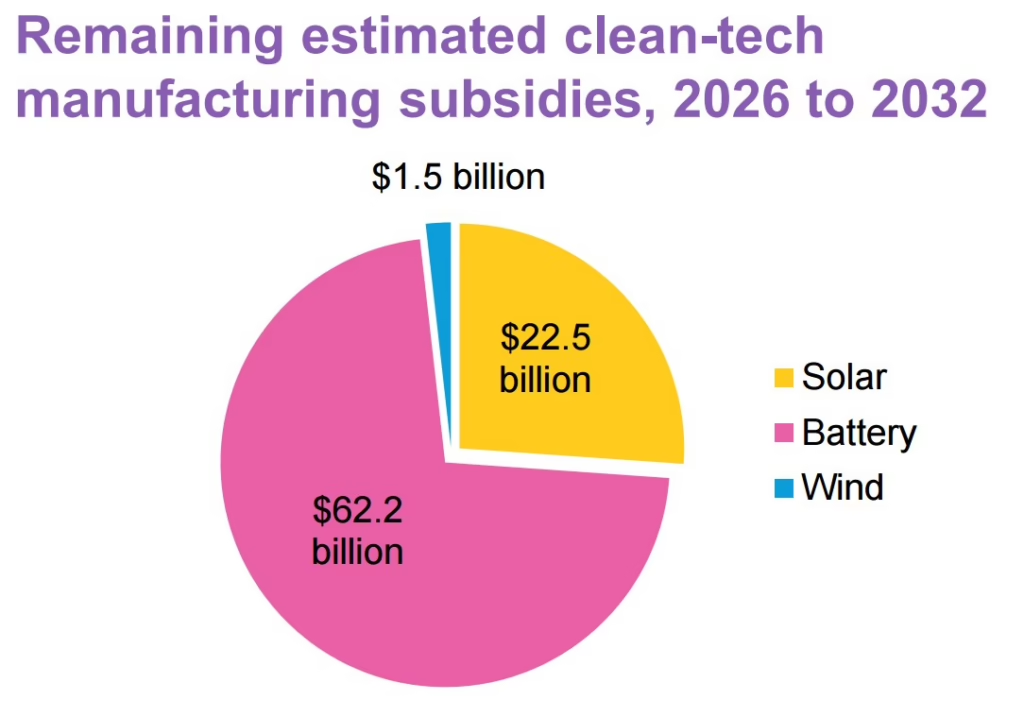

The Factbook said almost 10% of the $106 billion announced investment in clean-tech supply chains since the passage of the IRA has been cancelled following the rollback of incentives under the OBBBA.

Written by

")

Popular Posts