InfoLink reports BESS cell shipments of 202.3 GWh in first 3Q of 2024

The energy storage industry is steadily reshaping the global energy landscape, with a key analyst reporting lithium-ion battery shipments surpassing 202 GWh in the first nine months of the calendar year 2024, representing a 42.8% year-on-year increase. Notably, Q3 shipments rose by 16% quarter-on-quarter, marking a new record for a single quarter.

This has been driven by utility-scale solar, and gives insight into the the energy storage component of the global battery industry and also supplies electric vehicles.

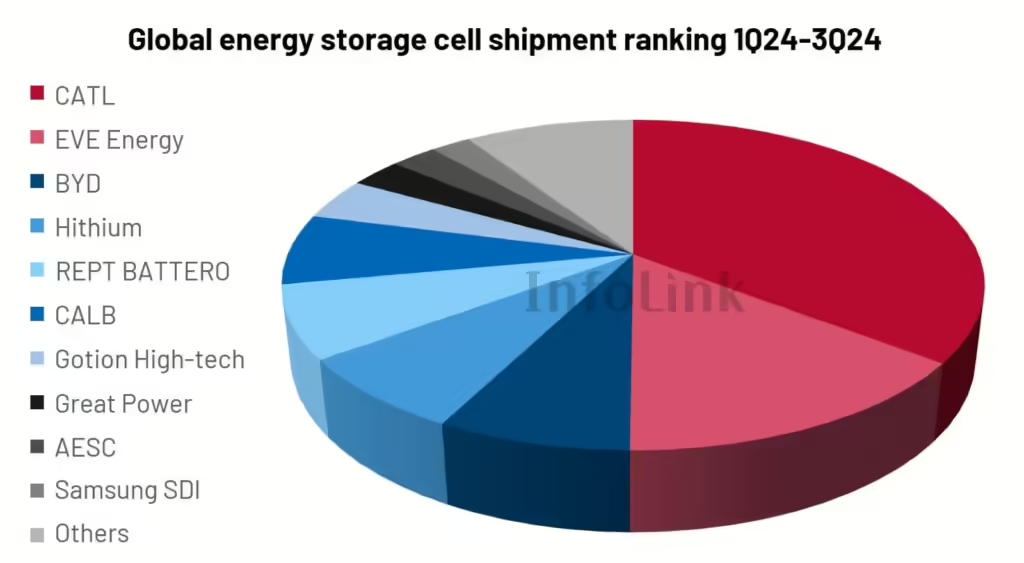

The industry remains highly consolidated, with the top 10 manufacturers capturing 90.7% of the market. China’s CATL continues to dominate, followed by EVE Energy, BYD, Hithium, and REPT BATTERO. CATL maintains its leadership through operational scale, while EVE Energy has secured its second-place position by partnering with key players like HyperStrong and Powin. Meanwhile, BYD has climbed to third place, bolstered by increased shipments to the Americas.

*Source: InfoLink’s Global Lithium-Ion Battery Supply Chain Database

*InfoLink aims for accuracy; however, in case of discrepancies, official manufacturer data shall prevail.

Competition remains fierce among the third to sixth-ranked players—BYD, Hithium, REPT, and CALB—whose market shares differ by less than 1%. South Korean manufacturers, including LG and SDI, have faced declining market shares as the industry transitions from nickel-cobalt-aluminum (NCA) and nickel-cobalt-manganese (NCM) batteries to lithium iron phosphate (LFP) technology, which dominates production in China.

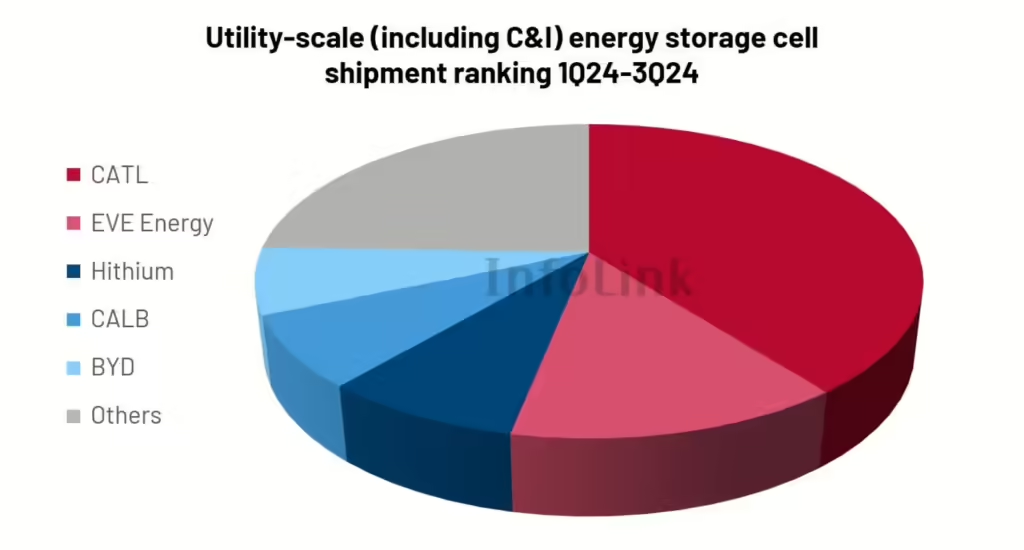

Utility-scale storage drives growth

Utility-scale storage continues to lead the market, with shipments reaching 180 GWh in the first three quarters—a 49.4% year-on-year increase. CATL and EVE Energy jointly hold nearly 55% of the market, while Hithium, CALB, and BYD each shipped over 10 GWh.

Large-capacity cells (300Ah+) accounted for 40% of Q3 shipments, reflecting their growing appeal. Although interest in 500Ah+ cells is rising, 300Ah+ cells are expected to remain the market standard until higher-capacity alternatives achieve broader validation.

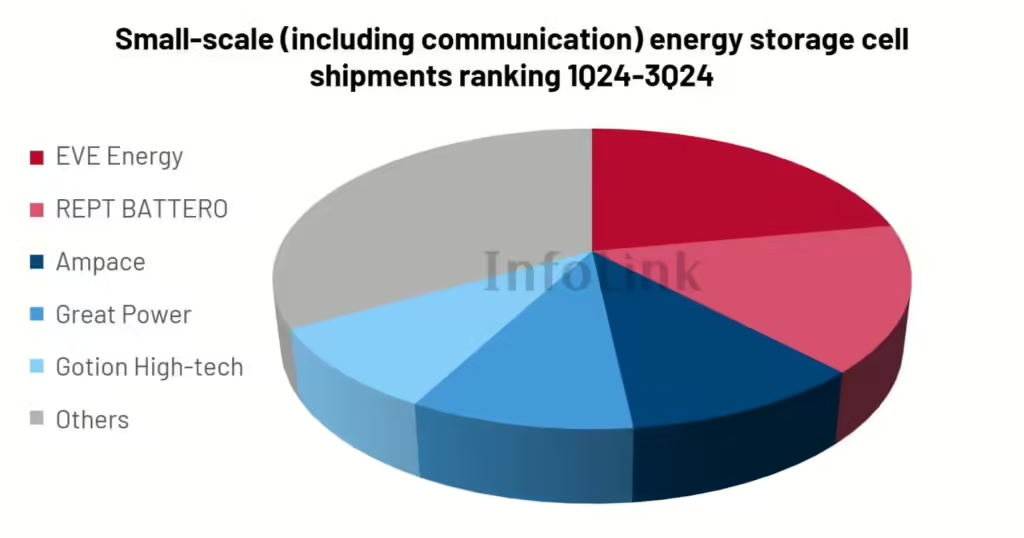

Small-scale storage expands to more regions

The small-scale energy storage sector also showed recovery, with shipments totaling 22.3 GWh during the first three quarters, up 5.2% year-on-year. EVE Energy and REPT are market leaders in this segment, though intensified competition has reduced the combined market share of the top five players to below 70%.

Demand has expanded beyond Europe and North America to include Asia, Africa, and Latin America, prompting manufacturers to adopt globally diversified strategies.

Outlook

InfoLink Consulting identifies both challenges and opportunities for the sector. Rising global policy risks call for greater operational resilience, particularly as policy shifts in key markets could impact growth trajectories. The report advises manufacturers to strengthen international operations to remain competitive.

Technological innovation and international expansion will continue to shape the industry, highlighting the need for adaptability in a rapidly evolving market. InfoLink’s findings underscore the importance of agility as manufacturers navigate this dynamic landscape.

Written by

")