California vs. Texas: A comparison of battery energy storage market participation

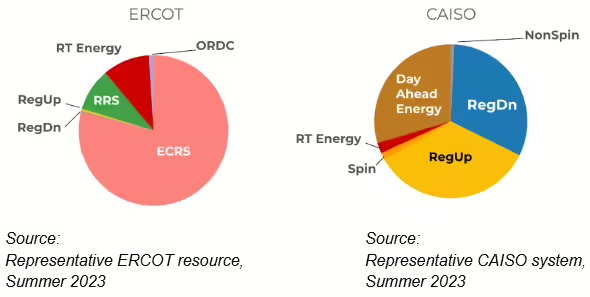

The first key difference between California and Texas is the revenue mix for battery systems. The graphs below compare the revenue mix for two representative systems.

Both markets share similarities in that their revenue streams heavily emphasize grid ancillary services. In ERCOT [the Electric Reliability Council of Texas], ECRS [the ERCOT Contingency Reserve Service, which ensures grid stability] was a major contributor due to high initial prices in 2023. Real-time energy accounted for just under 15% of prices while day-ahead energy prices played a minor role.

In CAISO [the California Independent System Operator], ancillary services contributed significantly but prices were lower than in ERCOT. Day-ahead energy constituted around 30% of revenue, with real-time energy contributing less. Since 2023, both markets have seen a trend toward more energy-driven revenues due to ancillary-service market saturation, driven by the low marginal costs of energy storage resources participating in the ancillary services markets.

Revenue sources

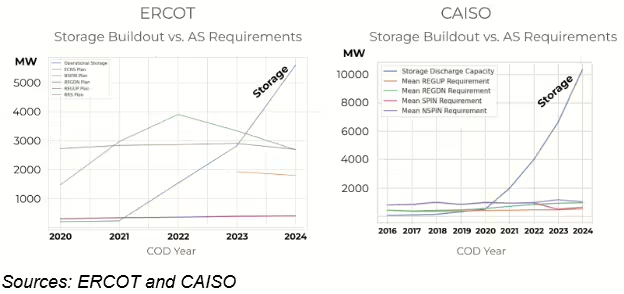

ERCOT and CAISO have distinct dynamics in storage capacity relative to ancillary service procurement.

In ERCOT (as shown on the graph pictured above, left), the addition of ECRS in 2023 led to a reduction in revenue derived from non-spinning reserve services [providing additional dispatchable capacity when real-time reserves are low] but still resulted in a net increase in ancillary services revenue. This, along with increased demand and a hot summer, led to ancillary service saturation not occurring in 2023, as many people had predicted in 2022.

For CAISO as shown in the graph pictured above, right, meaningful ancillary services revenue opportunities persisted in 2023 as storage buildout continued to grow and we saw ancillary services saturation occurring more fully in 2024.

Regional differences

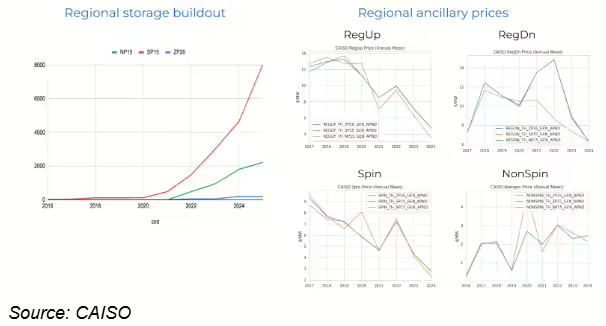

There are several reasons for the differences in ancillary service price saturation in CAISO, one of which is regional nuances. In ERCOT, ancillary services are procured systemwide. CAISO factors in intra-CAISO transmission constraints and procures ancillaries zonally, accounting for intra-CAISO transmission constraints.

Energy storage buildout in California has predominantly occurred in the SP15 (Southern California) service area, leading to regional price discrepancies, particularly in RegDn [regulation down] areas. These differences persisted until 2024 when increased storage was added in NP15 (Northern California) and ZP26 (Central California), reducing regional disparities.

CAISO factors

There are four factors that affect day-ahead market (DAM) participation by battery energy storage resources in CAISO:

- Resource Adequacy obligations: Most storage resources with RA [resource adequacy] contracts are required to bid into the DAM.

- Default Energy Bid (DEB) requirements: DEB requirements, designed to prevent price manipulation, can impact economic bids, particularly for batteries, where opportunity costs are high.

- State of Charge (SOC) rules: CAISO clears ancillary services awards based on SOC expectations. Energy storage operators must optimize for both what CAISO expects to happen and what they believe will actually happen, making DAM awards critical for ancillary revenue in CAISO, unlike ERCOT.

Opportunity costs: Bidding in the day-ahead market means sacrificing potential real-time opportunities, which always carry a chance of price spikes. In the real-time market that opportunity no longer exists, meaning the cost is simply idling. This distinction significantly affects bidding strategy in both markets.

Day-ahead energy constitutes a significant portion of CAISO battery revenue, unlike in ERCOT, where ancillary services dominate. In CAISO, obligations including RA contracts and DEB rules shape day-ahead bids, with batteries strategically managing SOC expectations. By contrast, ERCOT batteries primarily focus on ancillary services but are increasing participation in real-time and day-ahead markets.

CAISO day-ahead bidding

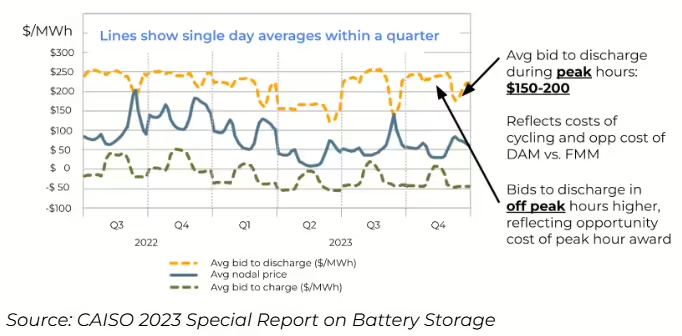

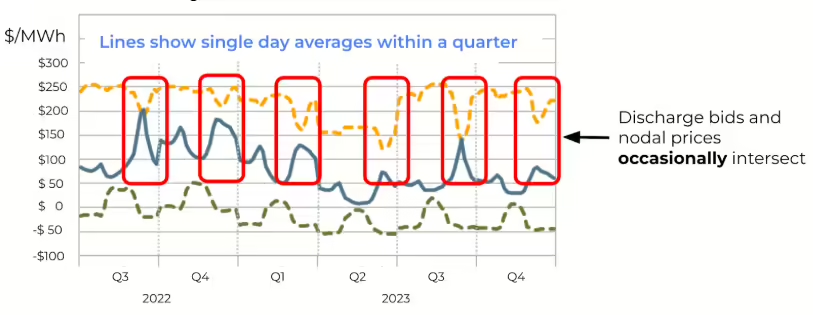

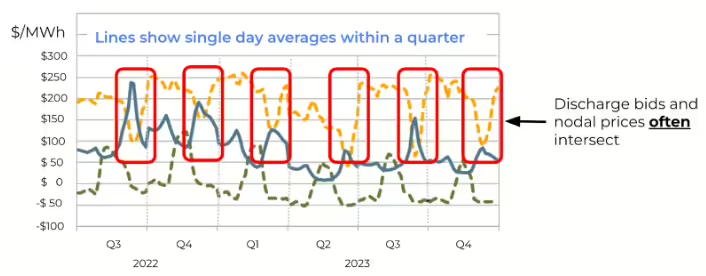

Finally, the CAISO day-ahead bidding landscape shows interesting patterns. The chart above shows the battery fleet-wide average values for a 24-hour period within each quarter. The first thing to note is that bids to discharge fall during the evening peak period. What’s happening here? Batteries are strategically using economic bids to avoid discharge during most hours except when peak prices make it worthwhile. During these peak periods, the price to discharge ranges from $150 per MW to $200 per MW. Conversely, the highest priced bids to discharge occur in the middle of the day, when batteries expect prices to be lowest, making it an ideal time to charge.

Where the charge and discharge lines intersect, this indicates that the average battery’s bids are clearing to either charge or discharge. Highlighting these intersections in the evening shows that discharge bids do occasionally overlap, leading to mixed behaviors where some batteries clear in the DAM while others do not.

15-minute market

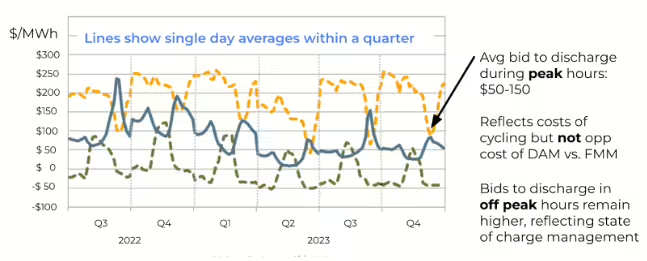

In the 15-minute market (FMM), the charts show similar patterns for discharge and charge bids but in a more pronounced way. The average bid to discharge during peak hours has decreased to between $50/MW and $100/MW. Unlike in the DAM, these batteries do not face opportunity costs of providing more valuable services, making them willing to discharge at a lower price in the FMM.

Examining the evening period, average bid prices often intersect average prices, indicating that batteries frequently clear a significant amount of capacity as a fleet for charging and discharging in the FMM.

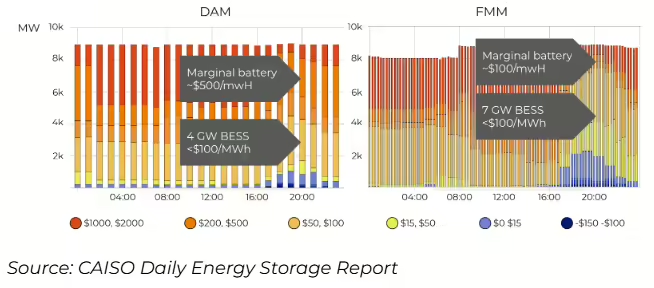

Let’s zoom in on a single day to examine battery behavior in more detail using CAISO data.

During hour 20, the arrows on the chart above highlight key differences between DAM and FMM bidding. In DAM, 4 GW of capacity bid below $100/MW, while the seventh GW priced around $500/MW. By contrast, in FMM, 7 GW of capacity bid below $100/MW, with the marginal battery around $100/MW. The DAM clearing price during this hour was around $500, compared to $100 in FMM, showing significant differences due to varying opportunity costs.

These differences indicate structural factors leading to distinct bidding behavior in the DAM and the FMM. On this day, it made sense for some batteries to bid in the DAM but these dynamics can shift, possibly leading to price spikes or shifts in delivery to the FMM.

To maximize revenue, forecasting behavior is crucial, especially given the dynamic nature of battery interactions between the DAM and the FMM. CAISO is the first US ISO demonstrating the impact that battery storage will have in setting marginal energy prices in both the DAM and the FMM, a new dynamic that market participants need to incorporate into their decisions. Advanced forecasting is key to understanding and optimizing this behavior.

ERCOT storage prices

Turning to ERCOT, we are beginning to see similar trends. In 2023, some 85% of battery revenue came from ancillary services. By 2024, that had shifted, with most batteries active in both the real-time market (RTM) for energy and the DAM. Battery storage is increasingly setting the marginal price in ERCOT’s RTM, with 55% of RTM intervals set by batteries in 2024. As battery capacity continues to grow, we expect increased DAM participation. We expect that ERCOT will see some of the same dynamics as CAISO, with energy storage setting marginal energy prices in the DAM and the RTM.

Conclusions

- ERCOT has followed CAISO in ancillary service pricing, though the trend has been inconsistent due to regional procurement differences and new products. This trend is likely to continue.

- CAISO batteries are significantly impacting the energy market and we expect similar impacts to emerge in ERCOT, moving forward.

- As batteries play unique roles in both day-ahead and RTMs, their bidding strategies will be crucial for maximizing revenue and influencing other market participants.

Key takeaway: Optimal storage market participation will require advanced forecasting of both the DAM and RTMs to determine the best opportunities for DAM participation.

About the author: David Miller is the chief commercial officer of Gridmatic, an artificial intelligence-enabled financial trader and battery optimizer in the DAM across ISOs. Gridmatic’s success in ERCOT is evidenced by public data, showing the company as the most profitable day-ahead energy trader since the company began trading in 2017.

Written by

")

Popular Posts