It’s high time for an EU Battery Storage Action Plan

Battery storage is the fastest-growing energy technology worldwide and is set to define the trajectory of the energy transformation going forward. Global investments in battery storage went from just $1 billion in 2015 to nearly $70 billion today, according to the International Energy Agency’s World Energy Investment 2025 analysis. This is despite the enormous 80% decrease in average selling battery prices since 2015.

Off their radar until recently, policymakers and investors have recognised the central role of batteries for the energy transition. Batteries are the absolute shortcut to delivering flexible and electrified energy systems across the globe.

The EU battery revolution

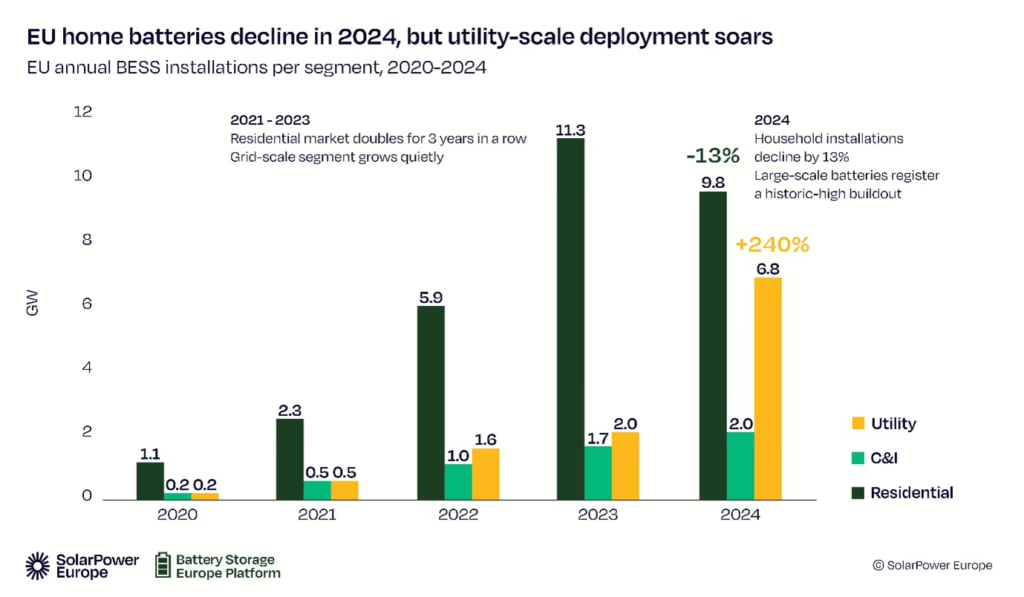

In the EU, the battery revolution started at the small-scale level, in times of crisis (2021-2023). In tandem with solar PV, the growth was driven by skyrocketing power prices and the desire to become self-sufficient, along with significant price reductions. The energy crisis shock was particularly strong in Germany, which rapidly became the top European market, with a consistent attachment rate of 70+%.

From 2020 to 2023, the EU home battery market doubled on a yearly basis and grew 11-fold from 1 GWh installed in 2021 to more than 11 GWh in 2023. Many countries, like the Czech Republic or Italy, provided households with the financial means to acquire solar+storage systems, with attractive CAPEX subsidies or tax incentives.

Over the same period, across the EU, large-scale systems were growing quietly, but steadily, increasing their annual market 10-fold. Without clear revenue streams and long permitting and grid connection procedures, project developments were slow and often delayed.

The C&I storage segment, unlike for solar, registered minor growth rates in the early 2020s, with very low attachment rates across the board (below 5%). The key factors were weak regulations, high grid charges, scarce financial incentives, slow permitting, limited industry knowledge, and few ways to combine revenue streams.

Shifting dynamics

In light of declining power prices and the phase-out of household support schemes, 2024 showed us yet again how quickly paradigm changes materialise on energy.

The residential BESS market registered its first decline in a decade in 2024 (-13%), which, despite being somewhat small, was widely felt across the industry given the high growth expectations of the energy crisis. Still, C&I batteries kept on growing, but remained below their true potential.

However, grid batteries finally had a watershed moment, delivering a record high level of installations, 3.5 times more than in 2023. Half was grid-connected in Italy, where projects contracted in past auctions were finally brought online. This is hard evidence that the technology is ready to be deployed at the scale the energy transition requires.

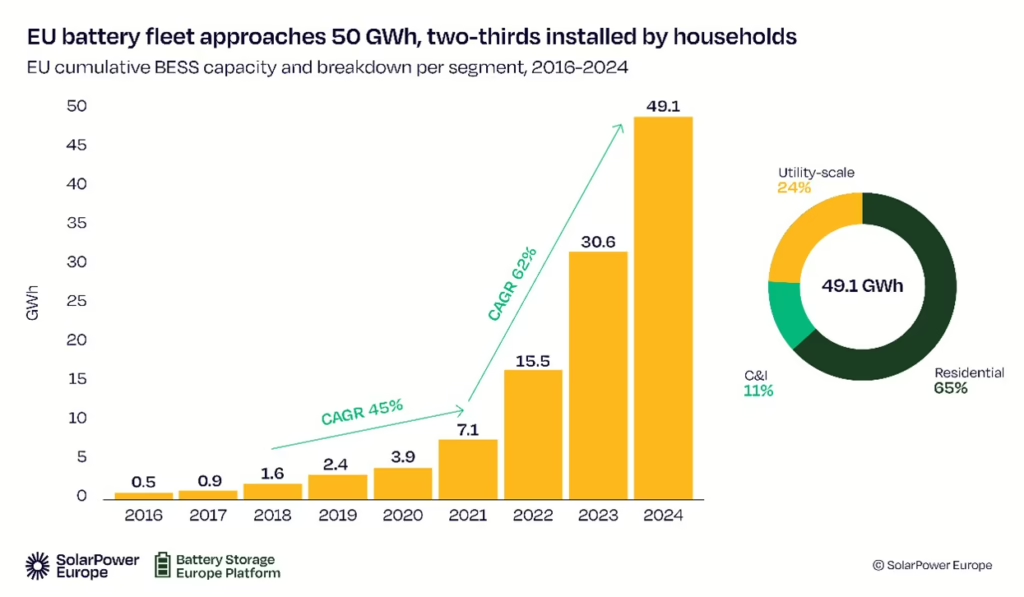

All in all, despite the slowdown, battery systems were again growing to new heights with 18.5 GWh added last year. This leaves the EU with nearly 50 GWh installed, 2/3 of which is residential capacity.

To put this into perspective, China has installed almost the same total capacity (53 GWh) only in H1 2025, while the US deployed 15 GWh in the first 6 months of 2025, according to Rho Motion’s grid-scale BESS database.

Consolidation, further growth and system requirements

2025 is poised to become the first year that grid batteries dominate deployment over the residential segment. This trend is expected to continue going forward, and the large-scale segment will reverse its weight on the mix by the end of the decade.

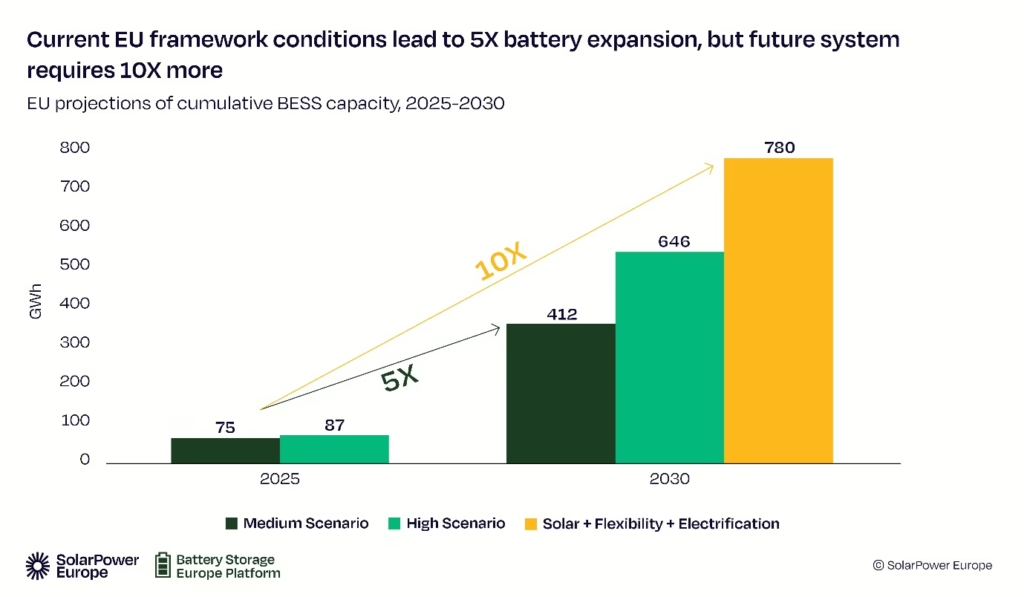

Projecting current market and policy conditions until 2030, shows that the battery fleet would grow 5-fold to over 400 GWh. Is this enough? According to our calculations presented in the Mission Solar 2040 report, the EU fleet has to grow more than ten times by 2030, if we are to make significant progress in our journey to a renewable-based energy system.

How do we get there?

If the EU needs to get above our High Scenario, that means we need to drastically improve the framework conditions for deployment.

Similar to the Solar Strategy, adopted in 2022, we call on the Commission to adopt a Battery Storage Action Plan for the EU. This plan should set ambitious deployment targets, outline a pathway to eliminate existing barriers, and develop an industrial strategy to support resilient and sustainable battery supply chains.

To accelerate the expansion of batteries, permitting procedures need to be streamlined, and grid connection needs to be facilitated. Key measures revolve around allowing developers to jointly submit permit applications for hybrid projects, or establishing differentiated queues for generation, standalone storage and demand.

Fire, noise, and safety requirements need to be harmonised across Member States. This will allow developers to establish a more standardised business model across geographies, while also guaranteeing secure and adequate deployment.

Batteries are also very well suited to deliver on energy security. Where EU countries have decided to create capacity markets, BESS should play a central role in decarbonising firm available power reserves.

Grid-stability services must also be opened for batteries in a market-based procurement format. TSOs should promote open competition for critical services like inertia, voltage control and black start capabilities, instead of relying on non-competitive mandates or grid-forming obligations for batteries.

On creating resilient supply chains, a suite of push and pull policies needs to be effectively rolled out to localise supply and create value in Europe. While providing CAPEX and OPEX support for producers is fundamental, no one will invest unless there is a clear route-to-market for EU-made equipment. A small but gradually increasing share of the market needs to be reserved to reward companies that produce and/or source locally.

Sustainability and end-of-life treatment should also be on the top of the EU agenda, and again, safety and quality. On ESG risks, the EU is already on the right direction in setting due diligence requirements, but EU companies require better guidance on how to meet them.

However, much more needs to be done, and that is why SolarPower Europe has created the Battery Storage Europe Platform, which brings together industry leaders to make battery storage and flexibility a political priority in EU energy and industrial policymaking.

About the author:

Antonio works at the Market Intelligence team of SolarPower Europe, specialising on energy storage. He focuses on storage markets, supply chains, and policy developments in Europe.

Written by

")