Baltic battery report: Get in if you can, says Aurora

For investors eyeing the Baltic states of Estonia, Latvia, and Lithuania, the message from AER is clear: timing is everything.

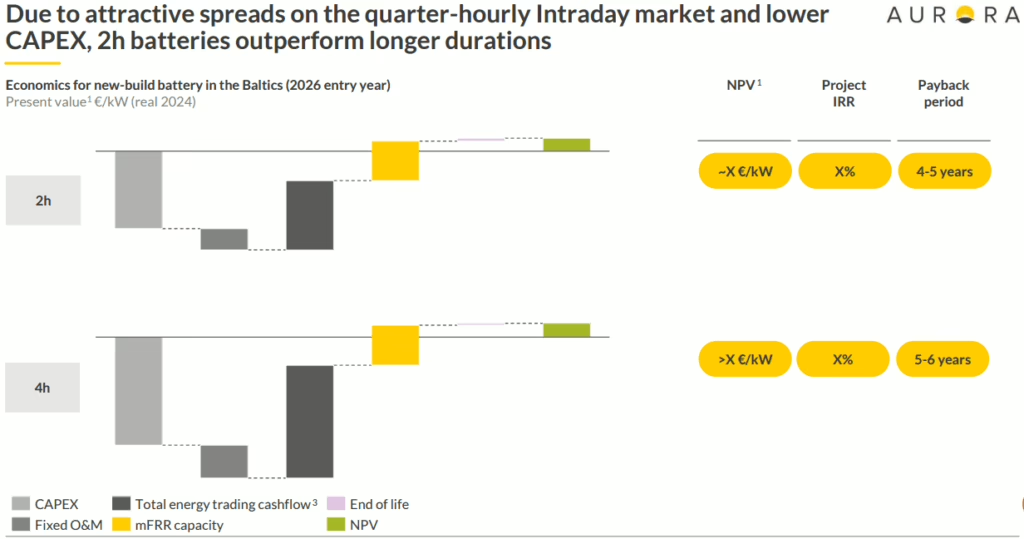

Battery storage investors in the Baltics face a narrowing window to capitalize on premium market conditions, says AER’s report. The profitability of projects is heavily dependent on their commissioning date, with early entrants benefiting from high prices on both manual Frequency Restoration Reserve (mFRR) capacity markets and significant spreads on the Day-Ahead and Intraday markets.

The analysis, based on a representative case for a standalone asset in Lithuania, shows a two-hour battery entering service in 2026 can achieve an Internal Rate of Return (IRR) of 13-16% and a payback period of four to five years. This even outperforms a four-hour system, which is projected to yield a still credible 11-15% IRR and a five to six year payback period over the same timeframe.

The advantage of the two-hour system stems from its lower initial investment cost or CapEx. While four-hour batteries can generate higher total margins, the increase is insufficient to outweigh the higher upfront capital expenditure. Furthermore, the two-hour battery is well-suited to capture value from the quarter-hourly granularity of the intraday market.

AER says the fast-mover advantage starts to erode quickly, and by 2029, the market landscape is expected to be different. The deployment of more flexible capacity in the Baltics is forecast to drive down both mFRR capacity prices and price spreads on energy markets. For projects commissioned in 2026, mFRR capacity reservations are a significant part of the revenue stack. For a 2029 entry, however, these revenues are expected to become only a small share of the total due to market saturation.

The project economics then shift: the same style of two-hour battery commissioned in 2029 is projected to see its IRR fall to a range of 6-13%, with the payback period extending to 7-10 years. The four-hour system would see an IRR of 5-12%. In this more competitive environment, energy arbitrage on the Day-Ahead and Intraday markets becomes a more critical component of battery revenue, and AER mentions needing to find “sharper optimization or multi-market stacking.” (See here, here, and here for recent coverage of optimizers).

Note that AER did not consider the automatic Frequency Restoration Reserve (aFRR) market in the Baltic region. While the analysts did not state the reasoning, the aFRR market is both more shallow and less mature than the mFRR market, both now and into the expected future. The pan-European aFRR platform (PICASSO) was delayed until March and April 2025, when Baltic TSOs fully joined the PICASSO platform.

Written by

")