Australian grid-scale battery storage earns $43.6M in Q4, 2024

The Australian Energy Market Operator (AEMO) has detailed in its regular quarterly reporting that grid-scale BESS output achieved new quarterly high net revenues.

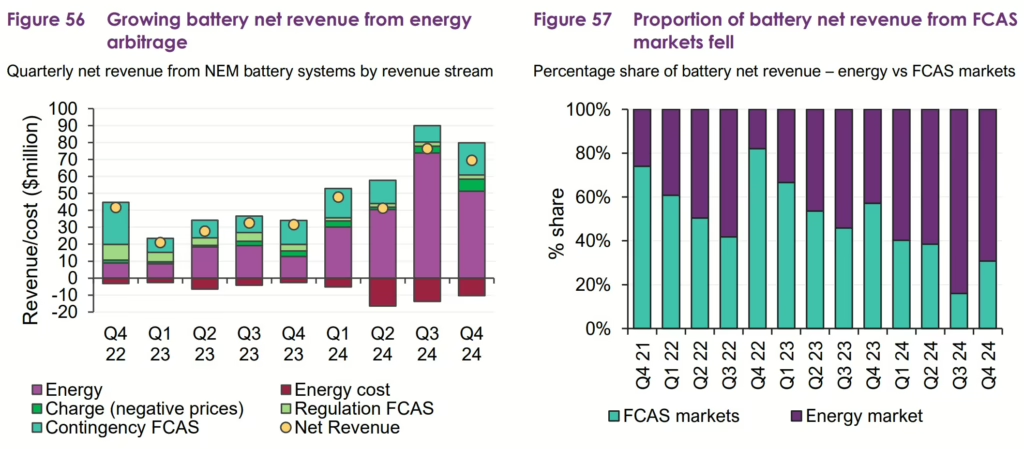

Reporting on the final quarter of 2024 of Australia’s National Electricity Market (NEM) energy flows and costs, AEMO’s report said the estimated net revenue for grid-scale batteries or big BESS, covering both energy and Frequency Control Ancillary Services (FCAS) markets, reached US$43.6 million (AU$69.5 million). Year-on-year, the rise is more than double Q4 2023 revenue of AU$31.5 million.

Regarding the components of revenue, the energy market net revenue increased by AU$34.6 million (up 257%) to a total of AU$48.1 million, representing 69% of revenue. The growth in energy arbitrage revenues largely came from energy generation, that is, discharging of batteries, growing at 300% year on year to AU$ 38.4 million.

Additionally, charging during negative price periods contributed an increase of AU$3.9 million, for a total of AU$7.2 million for the quarter. However, energy costs for charging above AU$0/MWh also rose substantially, reaching AU$7.7 million, a 298% increase.

Finally, FCAS contributed AU$21.3 for the quarter, up 19% or $3.4 million.

Breakdowns of revenues and comparisons to previous quarters are shown below from the AEMO report:

AEMO provided some narration to the data in the report, saying, quote:

- The rise in energy arbitrage net revenue across the NEM was driven in part by year-on-year increases in battery capacity driving higher availability and output in the energy market.

- NEM-wide average battery availability grew by 44%, from 755 MW in Q4 2023 to 1,087 MW in Q4 2024 (Figure 58).

- Battery generation averaged 90 MW this quarter, a 43 MW (+91%) increase compared to Q4 2023.

- The NEM-wide price spread for batteries averaged $243/MWh, up from $129/MWh in Q4 2023, reflecting increased high-priced volatility that saw battery operators capture more value during peak pricing events, particularly in the NEM’s northern regions.

In a media release, AEMO Executive General Manager – Reform Delivery, Violette Mouchaileh, noted the state of Western Australia saw falling coal generation partly thanks to energy storage, including battery contributions rising 1,400% via 425 MW of battery capacity being completed and participating in frequency co-optimised essential system services (FCESS).

“Increased battery storage in Western Australia helped the state hit a new quarterly average renewable contribution record of 46.4% and a renewable energy peak of 85.1%,” said Mouchaileh.

AEMO said the capacity of battery projects in the end-to-end connection process was 18.1 GW at the end of Q4 2024, an increase of 97% on the 9.2 GW at the end of Q4 2023. This includes projects in the “early stages” of development.

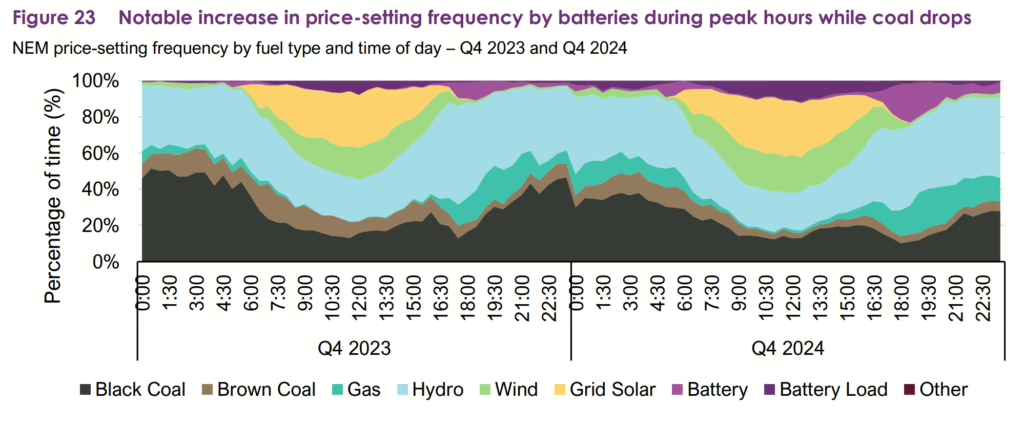

Detail on price-setting by generation type was also provided, with the chart showing the increasing penetration of batteries acting as the marginal generator, and generally, that batteries are increasingly influencing market prices, particularly during peak periods and most prominently between 4 pm and 8 pm, averaging 13%, up from 6% of recorded hours in Q4 last year.

Hydro storage, solar, curtailments

In terms of other energy storage sources, pumped hydro revenue rose to AU$83.3 million this quarter, up AU$54.5 million or 189%, through increased generation and volatility in Queensland and New South Wales. A single dam, Wivenhoe, in Queensland, saw its revenue rise AU$38.4 million.

The report noted that grid-scale solar output achieved a new quarterly high average on the NEM of 2.2 GW, an increase of 9% from 2023.

In terms of curtailments, grid-scale solar generation curtailments increased by 23 MW to 176 MW across the NEM, representing a 15% YoY increase.

- A focus on all things PV and renewable energy in Australia is always offered by partner site pv magazine Australia.

Written by

")

Popular Posts

")

")