Tariff uncertainty grips US battery development

Tariff chaos reigns supreme in the development of the US stationary battery energy storage industry. Facing extraordinary tariffs of 145% on BESS imports into the country, developers will have to rely on inventory to realize projects. When these stockpiles are exhausted the outlook is unclear.

Even the 145% tariff rate is uncertain. On April 14, the White House released a “Fact Sheet,” which appeared to clarify tariffs matters. In it, the White House noted that “China faces up to a 245% tariff on imports to the United States as a result of its retaliatory actions.” And it showed it is working. “This includes a 125% reciprocal tariff, a 20% tariff to address the fentanyl crisis, and Section 301 tariffs on specific goods, between 7.5% and 100%.”

Whether that means BESS will attract the 245% rate is unclear. Speaking at a Roth Capital Partners webinar on April 17, Daniel Finn-Foley of Clean Energy Associates (CEA) said that his team was still trying to ascertain whether BESS would be hit with the absurdly high rate.

“The numbers are just changing so quickly,” said Finn-Foley, the Director of Energy Storage, with CEA’s market intelligence team. But their impacts are already being felt.

Falling expectations

If the 145% rate sticks, it will still have a profound effect on the US BESS marketplace. And it comes on top of already reduced expectations given the uncertainty surrounding supportive policies such as the Investment Tax Credit (ITC) and the Production Tax Credit (PTC).

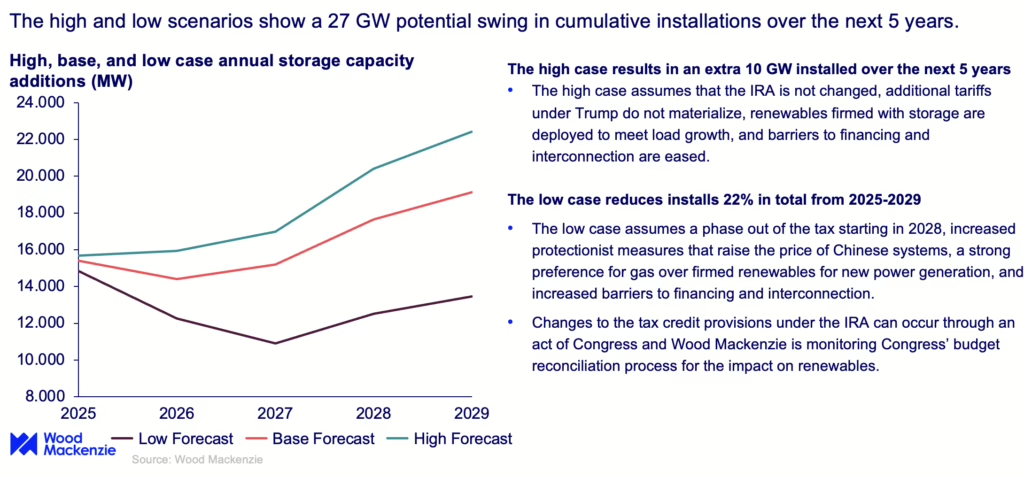

Energy analyst Wood Mackenzie forecast a 27 GW delta between its low and high scenario for BESS installations over the next five years. The high scenario was based on Inflation Reduction Act subsidies being retained, and that “additional tariffs under Trump do not materialize.” The low case now appears realistic, which forecasts a 27% decline in annual BESS installations in 2027 from today’s levels – to approximately 10.9 GW.

Allison Weis, the Global Head of Energy Storage for Wood Mackenzie told ESS News that while there are some robust drivers to BESS deployment including data center expansion and an expectation of load growth, she is antcipating “some definite delays past this year because of political uncertainty.”

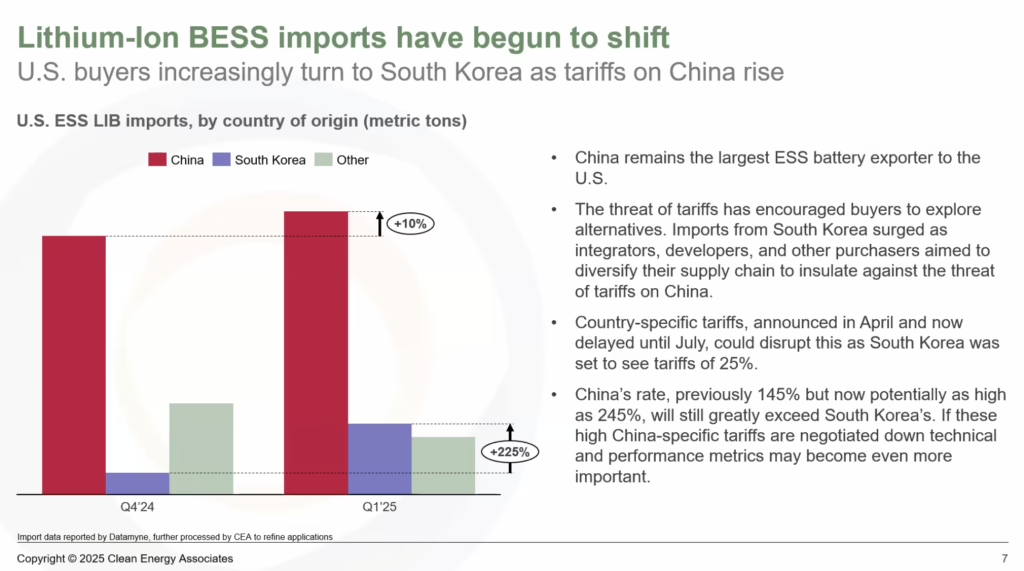

US market BESS deployments in 2025 look likely to be insulated by existing inventory, stockpiled in advance of the tariffs. CEA observes that lithium-ion battery imports into the US from China surged 10% from Q4 2024 to Q1 2025. At the same time, lithium-ion battery imports from South Korea and other sources, like Japan, surged by 225% in the same period. Finn-Foley said the trend is likely to continue as the implementation of the higher “reciprocal” tariffs on these countries has been delayed while Chinese tariffs remain prohibitively high.

“We may see some pullback [in project build out], but there’s enough capacity there so we are going to be insulated a little bit, meaning developers can ride it out until the new tariff landscape becomes clear,” said Finn-Foley.

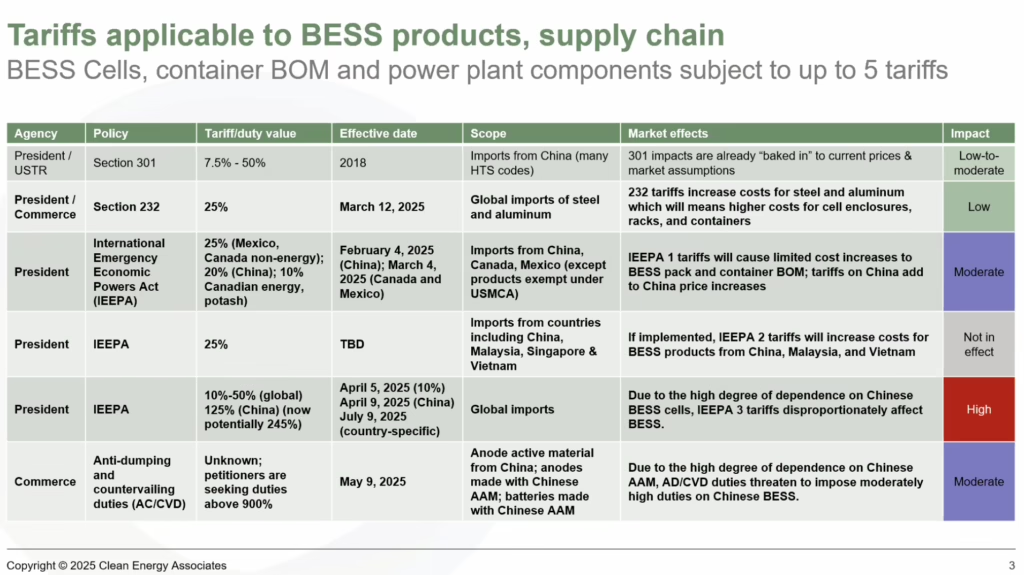

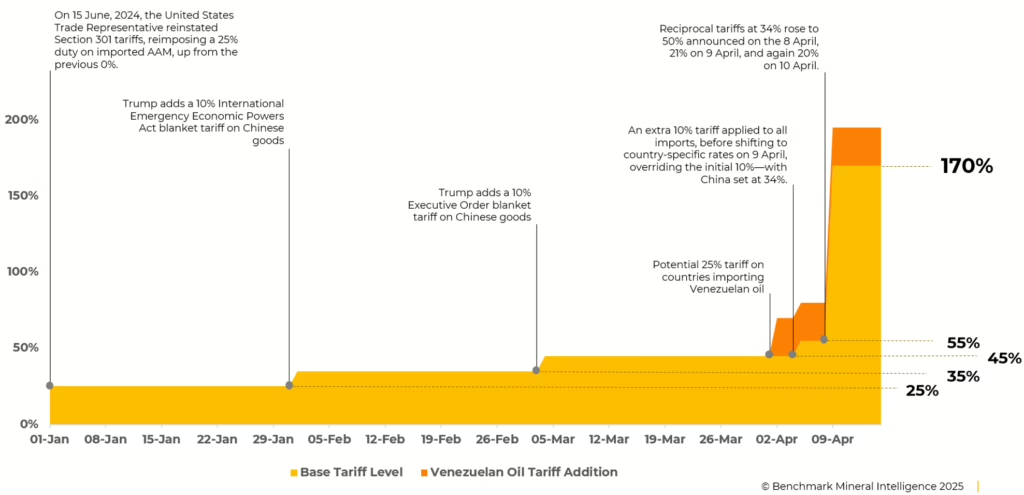

With the tariff measures somewhat of a moveable feast, they take some unpicking. CEA characterizes the recent bout of tariffs on Chinese goods, which were implemented under the auspices of the International Emergency Economic Powers Act (IEEPA) as IEEPA 1,2, and 3.

IEEPA 1 is the initial 20% “baseline tariff” on China; IEEPA 2 tariffs are those applied to countries that import Venezuelan oil, and is at the State Department’s discretion to implement and not yet in place; and IEEPA 3 Finn-Foley describes as the “big ones,” involving reciprocal rates that have escalated dramatically, as they relate to China, under what has quickly devolved into a tariff trade war. All of these measures are additive to earlier trade ones such as the Section 301 tariffs, Section 232 on steel and aluminium, and what are expected to be sizable anti-dumping and countervailing duties (AD/CVD) applied to battery active anode material.

The IEEPA tariffs are, said Finn-Foley, “beginning to make some of these earlier tariffs look relatively quaint.” Nonetheless, the anticipation of these measures were already driving accelerated installations in 2025, reports BloombergNEF.

“We expect late-stage projects rushing to commissioning before the scheduled increase in Section 301 tariffs to 25% starting next year to drive an annual addition this year,” Isshu Kikuma, an energy storage analyst with BloombergNEF told ESS News. In 2026, Kikuma said, BESS installations will “plummet,” due to the additional cost imposed by the array of tariffs.

Crunching the numbers, BloombergNEF said that a China tariff level of 145% would raise BESS prices to “the 2023 level.” Kikuma concluded that it would “discourage new investments and put the brakes on the growth.”

Manufacturing impacts

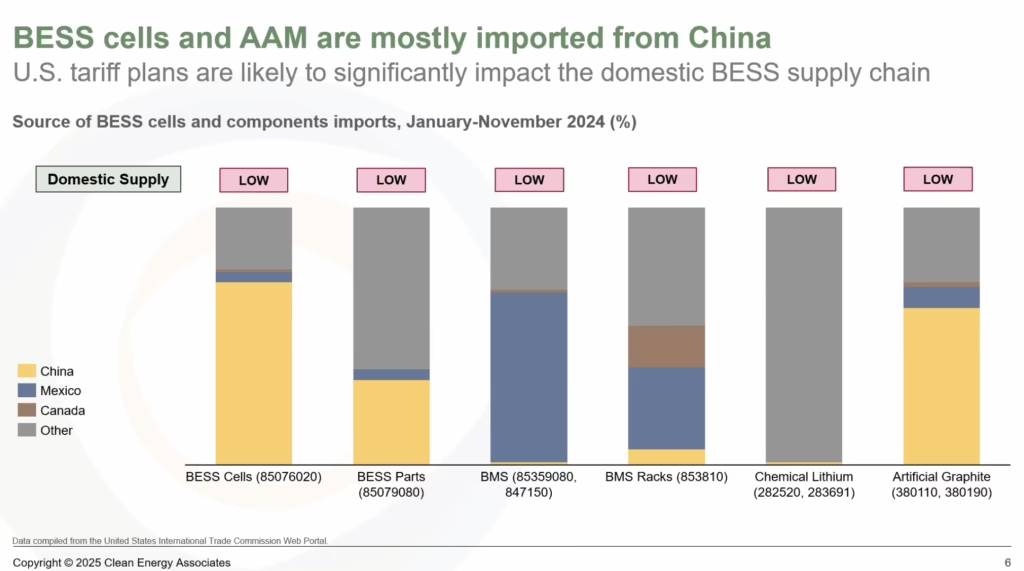

The tariffs will likely have significant impacts on the BESS supply chain. High tariffs on China will increase the competitiveness of lithium-ion batteries from South Korea and Japan – however producers in these countries could still face reciprocal tariffs, once they are unpaused. And here, the issue of battery chemistry comes into play.

Stationary energy storage applications have become dominated by lithium iron phosphate (LFP) batteries, which are used in more that 80% of stationary storage systems in the US at present. To supply the US market, South Korean and Japanese manufacturers would either have to make the substantial investment required to pivot to LFP, or convince buyers they can switch back to nickel manganese cobalt (NMC) chemistries.

“This is a big shift, from a pouch to a prismatic form factor, from NMC to LFP,” said Finn-Foley. “NMC has also been getting a lot of bad press over the last couple of months and years,” he added, referring to fires.

Chinese manufacturers could also relocate some production to Southeast Asia, although reciprocal tariffs apply here also. And it is not implausible that tariffs be extended on Chinese manufacturers if they relocate some operations to Southeast Asia, as has been the case with solar modules.

At first glance, the tariffs provide a tremendous boost to existing and prospective US BESS producers – and there are gigafabs under developed and integrator operations up and running. “Any sort of domestic supply chain you have in the US is going to be an advantage,” said Finn-Foley.

However, the lithium-ion BESS supply chain remains heavily dependent on China – from cells through to artificial graphite. In February, Benchmark Mineral Intelligence reported that Chinese suppliers produce around 80% of the world’s active anode material (AAM), and more than 90% of the synthetic graphite. And with these suppliers facing AD/CVD measures in Q3 2025, according to Benchmark Mineral Intelligence, costs are set to increase dramatically. And they will likely be additive to the existing tariffs.

In an analysis published last week on LinkedIn, Benchmark concluded that the duties would push imported AAM above the production costs and US facilities. However, US AAM production remains relatively nascent and there would remain a large “structural supply gap.”

“Bridging this gap will require significantly more investment in the domestic capacity pipeline,” concluded the Benchmark analysts – a dynamic that applies also to US battery integrators and prospective lithium-ion gigafab developers. The uncertainty unleashed on the market throughout April will severely undermine investor confidence. And BESS manufacturing operations are neither quick to establish nor cheap.

But it’s not all doom and gloom. Iola Hughes, the head of research at battery analyst Rho Motion, which was acquired by Benchmark in mid 2024, has struck a more moderate tone. Noting that BESS prices have halved over the past two years, that Chinese suppliers have “margin room,” and the fundamentals for deployment in the US remain strong, Hughes argued that the tariff numbers may “appear worse than it seems.”

“In the coming weeks, BESS market players will be reshuffling supply chains to mitigate tariff exposure,” Hughes wrote on LinkedIn. Although she acknowledged, “the market will face a tough balancing act in the short term.”

In terms of deployment, CEA’s Finn-Foley expects the project pipeline impacted by tariffs will likely be paused rather than canceled outright. “I think the storage industry can weather this. Can it weather 245% for the next 4-5 years? That is where we’ll see demand really slow down.”

More about

Written by

")

Popular Posts

")